The 5 Secrets of Successful Savers

Let’s face it: one of the biggest hurdles to buying property these days is scraping the money together for that hefty deposit – especially the 20% deposit most banks love.

Without the generosity of parents or a timely windfall, it’s harder than ever to get a foothold in many of Australia’s cities and regions, particularly for first home buyers.

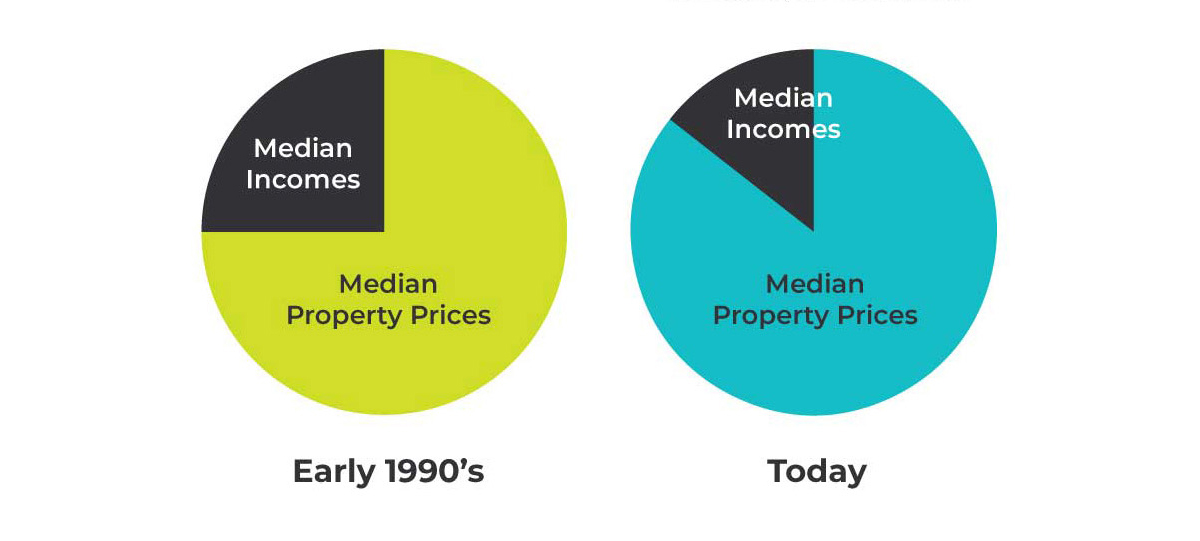

Here’s a fact*: Median property prices have increased from around 4 times median incomes in the early 1990s, to more than 7 times today.

To translate that into everyday speak, property prices have grown at eye-popping rates since the mid 1990s and incomes have simply not kept pace. So the gap between what the average Australian earns and the money they need to get on the property ladder is bigger than ever.

With this kind of market pressure, savers are winners! (And just by the way, there’s nothing a finance lender loves to see more than discipline with money and demonstrated savings).

So start cutting back on the retail therapy and stepping up these canny ways to build up your nest egg.

1. Consolidate any bad debt

Okay, there’s good debt and bad debt. Good debt is when you take out a loan to buy a well-chosen property; it’s a step towards securing your financial future. Bad debt is when you load up credit cards with frivolous purchases, take out a loan for a luxury car or holiday you can’t afford, and end up spending most of your salary servicing the high-interest debt you’ve drowning in.

Go visit your bank and see if you can consolidate any high-interest debt into a new loan with a modest interest rate. If all your credit cards are maxed out, investigate credit card balance transfer as a way to move from high-interest cards to a new card that offers a 1 or 2 year interest-free “honeymoon” period. Of course, none of this will work if you don’t take advantage of these interest-free periods to seriously whittle down your debt! Which leads to me to my next point…

2. Track your spending

Used wisely, credit cards are wonderful things, but their darker side is that they allow you to spend money willy-nilly, with no real idea of actually what your incomings and outgoings are. It’s no longer a case of, “when the money runs out, I’ll go without”; it’s more like a bottomless honey pot to keep dipping into. So the very first thing to do is itemise absolutely everything you’re spending money on each week. It will soon become very apparent where your money is going. Those late night online shopping binges; Friday office drinks that kick on till midnight; the gym membership you never use; endless take-away coffees and lunches … look at what’s getting you into debt and ask yourself, “Do I honestly need it?”

3. Draw up a budget

So now you’ve worked out where the leaks are, you need to plug them up, pronto! Separate out the necessities, from all that s**t you don’t need. Remember, you’ve got a goal now and you’re focusing on the bigger picture: like buying a property. Create a simple Excel spreadsheet to track your spending. Pack your lunch each day, cut out the Friday drinks, quit the binge shopping… By the time you’ve whittled back your spending to the bare essentials, you’ll hopefully find you now have money left over each week. Congratulations, you’ve made a conscious start.

4. Start saving

If you have bad debt, that’s the first thing you need to knock on the head. Then cut up the credit cards if you think there’s a danger you’ll relapse into bad habits. Set up a direct debit so at least 10% of your salary goes into your savings account before you have a chance to blow it, and then push yourself to put more money aside as you find new ways to cut costs and / or increase the incoming $$.

5. Be innovative and entrepreneurial

Once you start to see your savings build up, you’ll undoubtedly get more motivated. There’s all sorts of ways to push the envelope so the money pot grows faster. If you’re renting a place on your own, could you possibly house-share, if only as an interim thing to cut costs? Or maybe even move back home for a while? What about Airbnbing a spare room (with the landlord’s approval, of course)? Then there’s side gigs like driving an Uber or renting out your own car on one of the many car share apps available. Look hard enough and you’ll find all sorts of ways to boost your income.

As the saying goes, necessity is the mother of invention. And this exercise is all about YOU manufacturing the future you ultimately want for yourself. Go forth and prosper!